Property Development Finance Explained

Summary

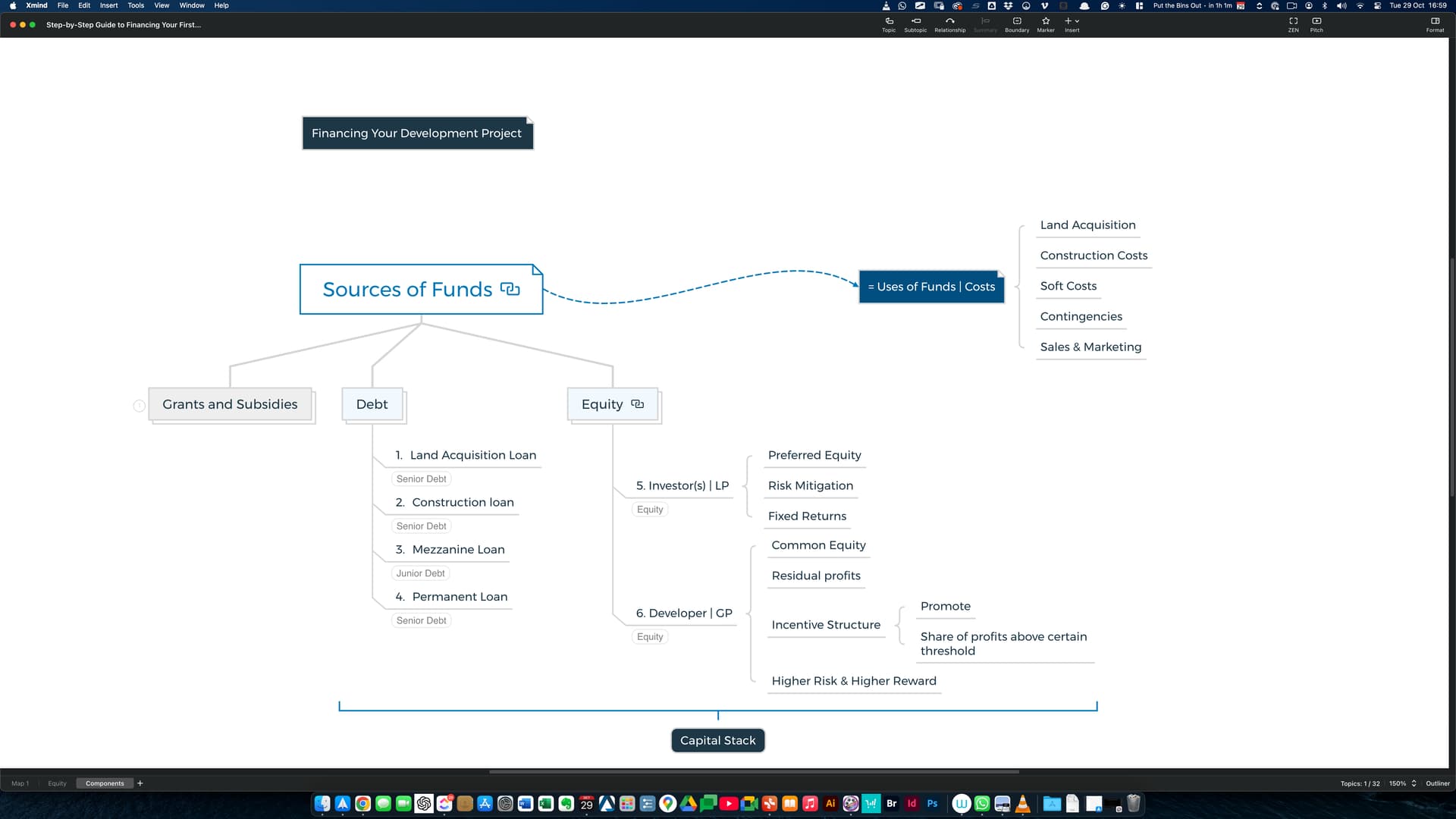

Sources and Uses of Funds

Sources and Uses of Funds

Key aspects in project financing are the sources (grants, debt, equity) and uses (costs), which must balance for feasibility.

Debt Structure

Debt Structure

Debt involves stages, starting with land acquisition loans, transitioning to construction loans, and sometimes permanent loans, especially for build-to-rent projects.

Equity and Preferred Returns

Equity and Preferred Returns

Investors receive preferred returns before developers, depending on their contributions, using cash flow waterfalls and incentive structures.

Capital Stack Importance

Capital Stack Importance

Capital stack includes all funding sources, prioritized from senior debts to equity, to protect lenders’ interests and mitigate risks.

Project Timeline Management

Project Timeline Management

Funds are allocated over timelines, with various loans and equity injections during different stages to cover costs and keep projects on track.

Promotional Offers

Promotional Offers

The video promotes resources like feasibility applications and developer communities for project planning and investment assessments.

Debt vs. Equity Ratios

Projects often use around 70% debt for construction costs, needing 30% equity to fill in, emphasizing the common industry approach for balancing risk and return.

Fixed Returns Example

A preferred return of 7% for investors is used, showing how fixed returns help in risk mitigation for high-contributing investors.

Project Timing

Construction phases can last several months, with loans like mezzanine loans often filling shortfalls as the project develops, showcasing the financial staging essential in development.

FAQs

1. What are the roles of different types of loans in a property development project?

-

Land Acquisition Loan: This is often the first loan in a project, providing funds specifically for purchasing the land. It covers the initial cost of securing the site, allowing the project to commence. This loan is considered “senior debt,” meaning it holds priority over others in repayment.

-

Construction Loan: After acquiring the land, a construction loan kicks in to fund building costs. It typically replaces the land acquisition loan, especially when the lender requires it to secure the highest repayment priority. This loan covers hard costs like materials and labor, and it’s also a senior debt, meaning lenders have the first claim on returns.

-

Mezzanine Loan: This is a “junior debt,” used when there’s a shortfall in funding. If the main loans don’t cover all costs (e.g., the bank funds only 70%, but 100% is needed), the mezzanine loan fills the gap, but at a higher interest rate. Due to its subordinate status, it’s repaid after senior debts, hence it’s riskier for the lender.

-

Permanent Loan: Often associated with build-to-rent projects, a permanent loan replaces the construction loan once the project is stabilized (achieving consistent rental income). This long-term loan allows the developer to retain ownership rather than sell, providing ongoing income through leasing.

2. How is preferred equity structured to mitigate risk for investors?

-

Priority in Cash Flow: Investors with preferred equity are paid before common equity holders (typically the developers). This means they receive returns from the project’s income before others, reducing their exposure to potential losses if project cash flow underperforms.

-

Fixed Returns: Often, preferred equity holders are promised a fixed return rate, like 7% as mentioned in the video. This fixed rate provides them with predictable earnings, even if the project’s overall profits vary. This stability is particularly attractive as it limits the risk of low returns associated with the inherent fluctuations in real estate markets.

-

Lower Risk, Lower Control: While preferred equity investors benefit from early payouts, they usually have less control over project decisions compared to general partners (developers). This trade-off offers them a lower-risk position since they’re not directly managing the project’s success but still enjoy an assured income stream.

-

Mitigated Downside and Structured Upside: Preferred equity arrangements often specify that any remaining profit, after meeting the preferred return threshold, is distributed based on pre-agreed ratios. If the project performs exceptionally well, preferred equity investors might receive additional returns based on their stake, enhancing their upside potential without increasing risk.

3. What distinguishes a build-to-rent from a develop-and-sell model in terms of funding?

Funding Structure

- Develop-and-Sell: This model focuses on completing the project and selling units quickly to recover costs and make a profit. The funding primarily relies on short-term loans, like land acquisition and construction loans, to cover immediate project costs. Upon selling the units, these loans are repaid, and any profits are distributed among the investors and developers.

- Build-to-Rent: In this model, the project is developed with the intent to retain ownership and generate ongoing rental income. Instead of aiming for an early sale, this model requires long-term funding strategies, like a permanent loan, which replaces the construction loan once the project is operational and generating rental income. This permanent loan allows the developer to refinance the construction loan with better long-term rates suitable for stable, income-generating properties.

Cash Flow Timeline

- Develop-and-Sell: Cash flow is focused on upfront sales, with income generated only after construction and sale. This model is sensitive to market conditions at the time of sale, as profits depend on the selling prices achieved upon project completion.

- Build-to-Rent: Here, the project generates continuous cash flow through rental income after construction. Since the developer isn’t focused on selling, they aim to achieve high occupancy rates to stabilize income over time, often taking a few years for rental income to reach its peak.

- Investor Returns and Loan Repayment:

- Develop-and-Sell: Once sales are completed, returns are distributed according to the capital stack, often prioritizing debt repayment, then preferred equity returns, followed by developer returns. The objective is to achieve profitability quickly for investors.

- Build-to-Rent: With rental income as the primary revenue stream, returns are typically slower but more predictable. This model may offer periodic income distributions to investors, and, over time, investors may receive a portion of the property’s value if it’s refinanced or partially sold. The permanent loan enables a consistent cash flow without needing to sell the property.